Inflation is one of those things Malaysians feel every day, even if they do not actively track it.

It shows up quietly. Your usual lunch costs a bit more. Your weekly grocery bill creeps up. Your monthly essentials feel tighter than they used to. Nothing feels extreme on its own, but over time, everything adds up.

As of early 2026, Malaysia’s headline inflation remains moderate, with inflation at 1.6% in January 2026 and 1.4% in February 2026. On paper, that sounds manageable. But many households still feel more pressure than those numbers suggest.

This is because inflation is uneven.

- Food-related spending still feels expensive

- Services like dining, insurance, and healthcare remain sticky

- Imported goods can be affected by currency movements

- Living costs often feel heavier in major urban areas where spending is already higher

So even if the headline inflation rate looks low, your real-life experience may feel very different.

Understanding inflation is not just about economics. It is about understanding why your money feels tighter and what you can realistically do about it.

(Source: Department of Statistics Malaysia; Bank Negara Malaysia)

What Is Inflation (And Why Should Malaysians Care)?

Inflation is the general increase in prices over time, which reduces how much your money can buy.

A simple way to understand it:

- You earn the same amount

- Prices go up

- Your purchasing power goes down

That means even if your salary does not change, your money buys less than before.

Inflation is usually measured through the Consumer Price Index (CPI), which tracks price changes across a basket of goods and services that households commonly spend on. In Malaysia, that includes categories such as food and beverages, housing and utilities, transport, healthcare, and education.

The CPI is useful, but it reflects the spending pattern of an average household. It does not perfectly match every person’s lifestyle or budget. That is why two households can experience inflation very differently.

Why should Malaysians care? Because inflation affects your ability to save, plan, invest, and maintain your standard of living over time.

(Source: Department of Statistics Malaysia; EPF Malaysia)

Why Inflation Matters More Than You Think

Inflation affects more than just prices. It affects your long-term financial stability.

It impacts daily spending

Most people feel inflation through recurring expenses such as:

- Groceries

- Eating out

- Transport

- Utilities

Even small increases matter when they happen every week or every month.

It erodes savings

If your money is growing slowly while prices keep rising, your savings lose real value over time. This is why long-term savers need to think beyond simply leaving cash idle.

It affects income growth

A pay raise does not automatically mean you are better off. If your salary grows more slowly than your cost of living, your real purchasing power still falls.

It complicates financial planning

Inflation makes it harder to estimate future costs, set realistic savings targets, and prepare for milestones like retirement, housing, or education.

(Source: EPF Malaysia; International Monetary Fund)

What Is Driving Inflation in Malaysia Right Now?

Malaysia’s inflation in 2026 is shaped by a mix of global pressures and local cost trends. While headline inflation remains moderate, price pressure has not disappeared. It is simply showing up unevenly across different parts of the economy.

Imported costs and currency movement

Malaysia depends on imported goods and inputs for parts of its food supply, consumer products, and business operations. When global prices rise or the ringgit weakens, some of those higher costs can filter into local prices.

Food supply and operating costs

Food remains a major part of household spending, so even small increases are widely felt. Higher production, transport, labour, and supply chain costs can all push food prices upward.

Services inflation

Some services continue to rise faster than headline inflation. Areas such as dining, insurance, healthcare, and education often stay elevated because they are tied to wages, administration, and ongoing business costs.

Domestic cost pressures

Even when global inflation cools, local costs still matter. Businesses may face higher wages, rentals, utilities, or compliance-related expenses, and some of those costs are eventually passed on to consumers.

Overall, inflation in Malaysia is not being driven by one single issue. It is the result of several smaller pressures happening at the same time.

(Source: Bank Negara Malaysia; Department of Statistics Malaysia)

How Inflation Affects Malaysian Consumers

For most Malaysians, inflation is less about economic theory and more about how far their money stretches each month. Even when the national inflation rate looks manageable, the day-to-day impact can still feel significant.

Everyday essentials feel tighter

Households usually notice inflation first in the things they buy most often, such as groceries, meals, transport, and household bills. These are recurring costs, so even modest increases add up quickly.

Fixed commitments become harder to manage

Expenses like rent, loan repayments, utilities, insurance, and childcare are harder to cut back on. When these costs rise, families have less flexibility in the rest of their budget.

Saving becomes more difficult

When more income goes toward essentials, it becomes harder to set money aside. This affects emergency savings, long-term goals, and overall financial confidence.

Lifestyle choices get squeezed

Inflation often forces households to adjust. People may eat out less, delay purchases, downgrade plans, or become more selective about non-essential spending.

Lower-income households feel it more strongly

The impact is usually harsher on lower-income households because a larger share of their income already goes toward necessities. That means they have less room to absorb rising prices.

In short, inflation affects consumers by quietly reducing financial breathing room. Even small price changes can reshape how people spend, save, and plan ahead.

(Source: Department of Statistics Malaysia; OECD; World Bank)

Why Inflation Feels Worse Than Official Numbers

Many Malaysians feel inflation more strongly than the official data suggests, and there are good reasons for that:

- The CPI is an average. It is designed to reflect an average household basket, not your exact monthly spending pattern.

- Spending patterns differ. If a large share of your budget goes to food, rent, transport, childcare, or healthcare, you may feel more inflation than someone who spends more on discretionary items.

- Essentials feel more painful. When necessities rise, you cannot easily cut them out. That makes inflation feel more immediate.

And finally, lower-income households are affected more heavily because a bigger share of their income goes toward basic needs. This means inflation can put more financial stress on B40 households than on higher-income groups.

(Source: Department of Statistics Malaysia; OECD; World Bank)

Who Is Most Affected by Inflation in Malaysia?

Inflation affects everyone, but not equally.

- B40 households usually feel the strongest impact because essentials take up a larger share of their income

- M40 households may feel pressure through lifestyle adjustments, reduced savings, or delayed goals

- T20 households are not immune, but they often have more financial buffers or assets to manage rising costs

This means inflation is not only an economic issue. It can also deepen financial stress across income groups, especially when essentials rise faster than expected.

(Source: Department of Statistics Malaysia; World Bank; OECD)

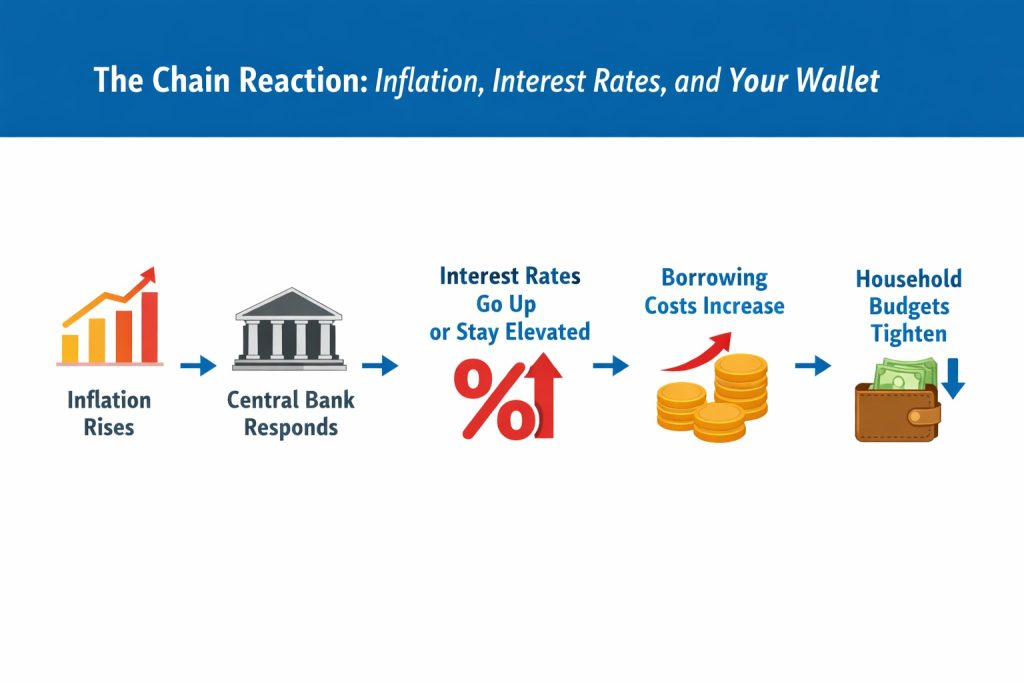

The Chain Reaction: Inflation, Interest Rates, and Your Wallet

Inflation also influences how money moves through the economy, especially through interest rates.

In simple terms, the chain reaction looks like this:

- Inflation rises

- The central bank assesses the outlook

- Interest rates may be increased or kept elevated

- Borrowing becomes more expensive

- Spending and demand may cool

In Malaysia, Bank Negara Malaysia kept the Overnight Policy Rate at 2.75% in its January and March 2026 decisions, while signalling that inflation should remain moderate overall. Even so, interest-rate expectations still matter because they affect borrowing, refinancing, and household confidence.

For consumers, this can mean:

- Higher financing costs

- More careful spending decisions

- Tighter household budgets when repayments feel heavier

(Source: Bank Negara Malaysia)

Real-Life Examples Malaysians Can Relate To

Inflation is easier to understand through everyday experiences.

Common signs consumers notice:

- Meals and drinks cost more than they used to

- Grocery bills stretch further than expected

- Insurance, healthcare, and transport feel more expensive over time

What these examples show:

- Small increases accumulate over time

- Daily expenses become harder to manage

- Financial pressure builds gradually

Inflation is not a one-time event. It is a continuous process.

(Source: Department of Statistics Malaysia; EPF Malaysia)

What Malaysians Can Do to Manage Inflation

While inflation cannot be controlled, its impact can be reduced with the right approach.

Step 1: Understand your spending

Break your expenses into:

- Fixed costs

- Variable essentials

- Discretionary spending

This helps you see where inflation is affecting you most.

Step 2: Adjust your budget

- Update your monthly numbers based on current prices

- Avoid relying on old assumptions

- Prioritise essentials first

Step 3: Protect your savings

- Avoid leaving too much money idle for long periods

- Consider savings or investment options that better preserve value over time

Step 4: Manage debt carefully

- Reduce high-interest debt obligations where possible

- Avoid unnecessary borrowing

- Focus on affordability, not just approval

Step 5: Plan for long-term resilience

- Build emergency savings

- Review your insurance and financial protection

- Look for ways to strengthen income over time

These are general financial tips for educational purposes and are not personalised financial advice.

(Source: EPF Malaysia; Bank Negara Malaysia)

Is Inflation Always Bad?

Inflation is not inherently negative, but it needs to remain controlled.

A stable and moderate inflation rate is generally considered healthier for the economy than either very high inflation or persistent deflation. Moderate inflation can support spending, business activity, and wage adjustments. But when inflation becomes too high, too broad, or too unpredictable, it starts to reduce purchasing power and create uncertainty for households and businesses.

So the real issue is not inflation existing at all. It is whether inflation stays manageable.

(Source: International Monetary Fund; Bank Negara Malaysia)

Understanding and Adapting to Inflation

Inflation in Malaysia in 2026 is not extreme, but it is clearly present in everyday life. Official figures show that headline inflation remains moderate, yet many households still feel pressure through food-related spending, services, healthcare, and other essential costs.

Understanding how inflation works helps you make better financial decisions and avoid being misled by headline numbers alone. When you understand why your money feels tighter, you are in a better position to budget, plan ahead, and protect your financial stability.

If your brand needs to explain complex topics like inflation in a way that resonates with Malaysian consumers, PRESS PR Agency can help turn insights into clear, relatable messaging that builds trust and credibility. Don’t hesitate to contact PRESS, Malaysia’s number one PR agency, and get your message heard by the right audience today!

Disclaimer: This article is for general informational purposes only and does not constitute financial, investment, or economic advice. Inflation affects households differently, so readers should consider their own financial situation before making money-related decisions.

{kind=link}