Paid up capital is one of those terms that shows up during incorporation…and then confuses people for years.

Many Malaysian founders assume it’s:

- a fixed legal requirement,

- a scorecard of how successful the business is, or

- a vanity number you bump up to “look established”.

In reality, paid-up capital is simpler and more practical than that.

It’s a record of how much real money shareholders have put into the company, and a quiet but important signal for banks, regulators, and partners.

With MSMEs contributing roughly 40% of national GDP, every new Sdn Bhd has to decide, “How much capital do we start with?” This guide shows how to answer that question in 2026, in plain language.

What Is Paid-Up Capital?

Paid-up capital is the amount of money shareholders have actually paid into the company in exchange for shares. Once that money is paid in, it belongs to the company.

On your balance sheet, it sits under equity. It is:

- not revenue,

- not profit, and

- not a direct measure of performance.

Issued Capital vs Paid-Up Capital (and the end of “authorised capital”)

Two terms matter today:

- Issued share capital – the total value of shares the company has issued to shareholders

- Paid-up capital – how much of that has actually been paid for

Historically, companies also stated authorised share capital (the maximum they could issue). Under the Companies Act 2016, that concept has been abolished. New Malaysian companies focus on issued and paid-up capital only.

Why Paid-Up Capital Matters in Practice

There’s no general statutory minimum, but paid-up capital still influences how others see your company.

1. It Signals Commitment

Paid-up capital shows how much real money the owners have put at risk. A services company with RM50,000 paid-up capital feels more serious than one with RM2, even if both are new.

2. It Affects How Banks View You

Banks care most about:

- Cash flow

- Repayment ability

- Management quality

But paid-up capital still enters the picture, especially for young businesses.

Typical Malaysian rules of thumb:

- RM1,000–RM10,000 – looks minimally serious for simple service businesses

- RM10,000 and above – more comfortable if you plan to seek loans or trade facilities

Not hard rules, but realistic expectations.

3. It Shapes Commercial Credibility

Suppliers, landlords, and partners often look at paid-up capital when deciding:

- Credit terms

- Rental deposits

- Contract length

Very low capital can trigger “shell company” or “fragile business” concerns.

Read More: https://www.press.com.my/business/new-business-malaysia-what-to-know/

4. It Links to Tenders, Licences, and Vendor Onboarding

Many tenders and licences build minimum paid-up capital into their criteria, for example:

- Construction (CIDB) – minimum paid-up capital increases with contractor grade and tender size

- Courier / postal licences – class-based thresholds, commonly from around RM100,000 upwards

- Oil & gas / energy vendors – some schemes expect RM100,000+ paid-up capital just to qualify

Even if your company law minimum is RM1, your sector may demand much more.

Legal Context in Malaysia (2026)

For private companies (Sdn Bhd):

- Under the Companies Act 2016, there is no statutory minimum paid-up capital

- You can legally incorporate with RM1 paid-up capital

- Companies Commission of Malaysia (SSM) will register the company if other requirements are met

However:

- Banks may view RM1 capital as a red flag

- Tender and vendor systems often build in their own minimums

- Sector regulators (e.g. construction, courier, certain foreign-owned setups) may explicitly require higher paid-up capital

Bottom line: RM1 is legal, but often impractical once you move beyond basic operations.

Key Things Business Owners Should Understand

1. Paid-Up Capital vs Cash in the Bank

When shareholders inject capital, the company:

- increases its paid-up capital (equity), and

- receives cash, which it can spend.

Even if the cash is fully used for legitimate expenses, the paid-up capital number stays in your records unless you formally reduce capital. Don’t confuse “starting capital” with “current bank balance”.

2. Paid-Up Capital vs Profit (and Tax)

- Paid-up capital is shareholder equity

- Profit is what’s left after revenue minus expenses

- Corporate tax is charged on profit, not paid-up capital

A company with RM5,000 capital and strong profits can pay more tax than a company with RM500,000 capital and weak profits. Authorities and auditors do not treat capital injections as income.

3. Paid-Up Capital vs Shareholder Loans

Two common ways to inject money:

Paid-up capital

- Strengthens equity permanently

- Viewed more positively by banks and some regulators

- Harder to withdraw without formal processes

Shareholder loans

- More flexible and repayable

- Can be subordinated to bank loans

- If large, may make the company look more leveraged

Many founders use a mix: a solid base of paid-up capital plus shareholder loans for extra flexibility.

Concrete Malaysian Examples

Example 1: SME Going for a Bank Facility

A small services Sdn Bhd has:

- RM50,000 paid-up capital

- Steady cash flow

- Clean records

When applying for a working capital line, the bank leans mainly on the cash flow and business track record, but the paid-up capital figure helps show the owners are committed and can absorb some volatility.

Example 2: Regulated Tender

A contractor wants to bid for larger projects. To qualify for a higher CIDB grade and related tenders, they must:

- meet the minimum paid-up capital threshold for that grade, and

- maintain it going forward.

If their capital is too low, they’re blocked at the registration stage, regardless of experience.

How Much Paid-Up Capital Is “Enough” in Malaysia?

There is no one-size-fits-all answer. You should align paid-up capital with:

- business model and cost structure,

- risk and asset intensity,

- licences and tenders you need, and

- your growth stage.

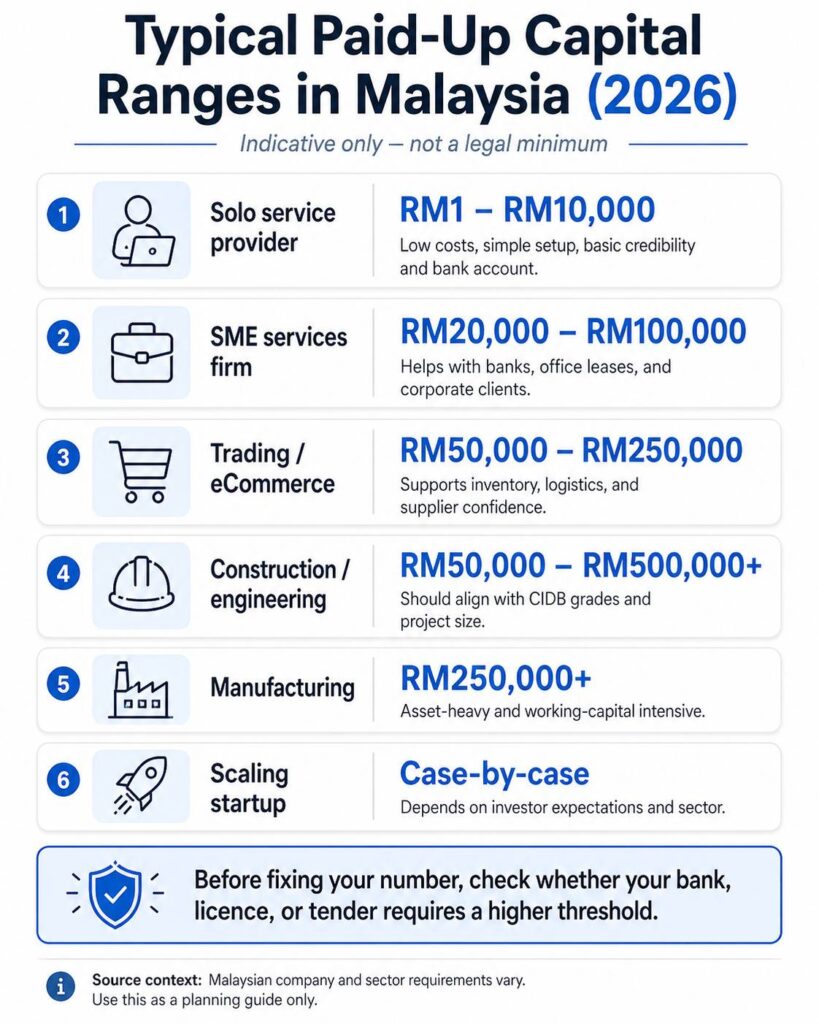

Practical Guidance Table (Indicative Only)

These ranges reflect common practice, not legal rules.

| Business Type | Typical Range | Why It’s Reasonable |

|---|---|---|

| Solo service provider | RM1 – RM10,000 | Low costs, simple setup, mainly for basic credibility and bank account. |

| SME services firm | RM20,000 – RM100,000 | Helps with banks, office leases, and corporate clients. |

| Trading / eCommerce | RM50,000 – RM250,000 | Inventory, logistics, and supplier confidence; can be higher for foreign-owned or licensed operations. |

| Construction / engineering | RM50,000 – RM500,000+ | Must align with CIDB grades and project size. |

| Manufacturing | RM250,000+ | Asset-heavy and working-capital intensive, with closer bank scrutiny. |

| Scaling startup | Case-by-case | Driven by investor expectations and sector (e.g. fintech, healthtech, logistics). |

Before fixing your number, check if banks, licences, or tenders you care about have specific capital thresholds.

Common Paid-Up Capital Myths

Myth 1: “Higher Capital = Guaranteed Loan Approval”

Reality: A higher equity base helps, but banks, guided by Bank Negara Malaysia, prioritise:

- cash flow,

- repayment ability,

- credit history, and

- business viability.

Capital is one piece of the risk picture, not a magic key.’

Read More: Anti-Profiteering Act Malaysia: Business & Consumer Guide

Myth 2: “Paid-Up Capital Must Stay in the Bank”

Reality: There is no legal requirement to freeze paid up capital in your bank account. Once injected, it can be used for legitimate business expenses. The important part is that it was genuinely paid in and properly recorded.

Myth 3: “More Paid-Up Capital = Higher Tax”

Reality: Paid up capital does not directly change your tax rate or increase your taxable income. Tax follows profit, not how much capital shareholders injected.

When Should You Increase Paid Up Capital?

Consider increasing paid up capital when you are:

- Expanding – entering new markets, hiring more staff, or taking on larger contracts

- Chasing licences or tenders – and you need to meet a specific capital threshold

- Preparing for bank financing – to present a stronger equity base

- Bringing in new shareholders – via new share subscriptions

Avoid increasing capital just for “nice big numbers” on paper. Make sure the amount supports a real business goal.

Making Paid Up Capital Work For You

Paid up capital is not a vanity metric or a compliance box. It’s a structural signal of how much real commitment your shareholders have made, and whether your company looks credible to banks, regulators, and commercial partners.

For Malaysia’s millions of registered businesses, getting this number right at incorporation (and updating it smartly as you grow) can make the difference between being seen as a fragile shell and a serious, durable company.

At PRESS PR Agency, Malaysia’s trustworthy PR agency, we help you turn structural signals like paid-up capital into real-world trust, through SEO, content, and digital positioning that make your company profile work harder for you.

Disclaimer: This article is for general information only and does not constitute legal, tax, or financial advice. Requirements can vary by sector and change over time. Always consult a qualified professional before deciding on your company’s share capital, licences, or financing structure.

- Companies Commission of Malaysia (SSM) — Companies Act 2016 (Act 777)

- Companies Commission of Malaysia (SSM) — FAQs on Companies Act 2016 & Transitional Issues (Policies/FAQ) — practical interpretations, including removal of the “authorised capital” concept.

- Department of Statistics Malaysia (DOSM) — Micro, Small & Medium Enterprises (MSMEs) Performance 2024

- Inland Revenue Board of Malaysia (LHDN/IRBM) — Tax Rate of Company

- Inland Revenue Board of Malaysia (LHDN/IRBM) — Public Ruling on tax treatment for micro, small and medium companies

- Bank Negara Malaysia (BNM) — Credit risk / prudential guidance for lending

- Malaysian Communications and Multimedia Commission (MCMC) — Licensing Guidelines

- Construction Industry Development Board (CIDB) Malaysia — Contractor registration requirements / grade framework materials

- OECD / Malaysia Competition Commission (MyCC) — Competitive Neutrality Reviews: Small-package delivery services in Malaysia

Frequently Asked Questions About Paid Up Capital

What Is Paid-Up Capital in Malaysia?

It’s the amount shareholders have actually paid into the company in exchange for shares. It appears under equity on the balance sheet and represents real owner commitment.

Is There a Minimum Paid Up Capital Requirement?

For private companies under the Companies Act 2016, no general statutory minimum applies. You can legally start with RM1. But banks, licences, and tenders may expect or require more, depending on your sector.

Does Higher Paid Up Capital Help With Loans?

It can improve credibility and your equity base, which helps. But approval mainly depends on cash flow, repayment ability, and overall risk, not just capital alone.

Can Paid Up Capital Be Used for Daily Expenses?

Yes. Once paid into the company, it can be used for any legitimate business purpose: salaries, rent, marketing, inventory, and so on.

Is Paid Up Capital the Same as Company Profit?

No. Paid-up capital is shareholder equity. Profit is what remains after deducting expenses from revenue. You can have high paid-up capital and losses, or low paid-up capital and strong profits.

When Should a Company Increase Paid Up Capital?

Common trigger points include preparing for expansion, meeting licensing or tender requirements, getting ready for bank financing, or bringing in new shareholders. If you’re unsure, speak with your company secretary, accountant, or corporate lawyer to model different scenarios.

{kind=link}