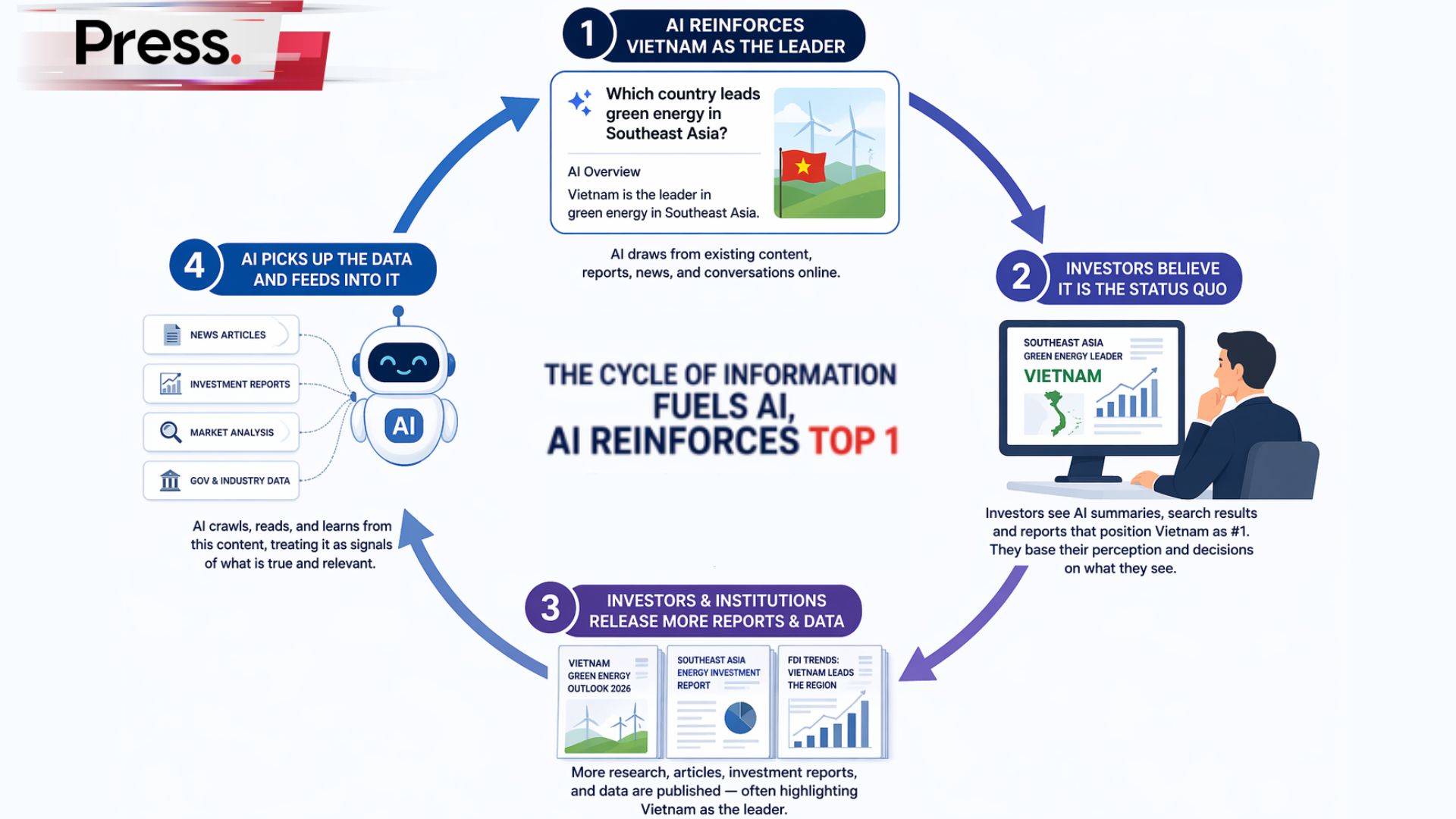

Ask any AI system or Google today “which country leads green energy in Southeast Asia”, and you’ll almost always hear the same answer, Vietnam.

Push a little further, and Indonesia or Thailand usually enters the conversation. Malaysia, despite everything it has built over the past decade, tends to sit in the background despite our efforts.

Now, that might sound like a branding issue, something for PR teams to fix.

But for policymakers, GLCs, and investment bodies, this is a marketing, branding and a everything issue.

Because today, global investors don’t start with consultants or site visits. They start with search results, AI summaries and what market analysis blogs say.

And in that layer, Malaysia is not showing up the way it should for FDI. So let’s talk about it.

Why AI Citation and Visibility Matters for Malaysia Policy Making

Let’s be frank here. The people searching for Southeast Asia’s green energy leader are usually not Malaysians, or even people from the region.

They are more likely to be:

- European manufacturers under ESG pressure

- Middle Eastern investors reallocating capital

- Chinese firms looking for the next ASEAN production base

- Multinationals assessing where to place future factories, plants, or supply chain operations

That matters because their first layer of due diligence is now digital.

“According to Bridgewise’s 2026 State of AI for Wealth findings, 78.3% of respondents already use AI tools for investment-related queries. And 65% said they’re likely to replace some of their existing investment research with AI in the coming year. If the LLM doesn’t see Malaysia’s Green Energy progress, the investor doesn’t see the opportunity.”

Investors are scanning:

- Search results

- AI summaries

- Global media coverage

- Investor-facing energy and infrastructure reports

As the leading Digital PR Agency, we know full well that when an entity like a country keeps showing up as the “leader” and AI starts reinforcing that narrative, the market starts making assumptions and assumptions become the dominant narrative.

What “Leader” Status Signals to Investors

When Malaysia is not mentioned, and Vietnam is, the message investors take away is often bigger than the headline itself.

They tend to assume that the leading country already has:

- Government backing: Policy direction is stable and long term

- Economic momentum: New industries, suppliers, and downstream opportunities are already forming

- Infrastructure readiness: Grid, transmission, and execution environment are already there

These assumptions are not always perfectly accurate, but they influence investment behaviour anyway.

And that is exactly why visibility matters.

Read more: Why Businesses Need To Support Malaysian Sustainability

Malaysia Has the Substance, But Not the Narrative

This is where the disconnect becomes frustrating.

Malaysia is not short on green energy ambition, far from it. In fact, Malaysia has built one of the more ambitious transition systems in the region, supported by major national programmes and long-term planning.

Major Green Energy Initiatives Malaysia Already Has

Each of these programmes is publicly documented by SEDA, the Energy Commission (ST), and TNB.

| Initiative | What It Does | Why It Matters for Investors |

|---|---|---|

| NETR (National Energy Transition Roadmap) | Long-term national strategy targeting net zero by 2050 | Signals policy stability, long-term direction, and government commitment to energy transition |

| LSS (Large Scale Solar) | Competitive bidding for utility-scale solar farms | Enables large-scale deployment, creates bankable solar projects and long-term asset opportunities |

| NEM (Net Energy Metering) | Allows businesses and households to offset electricity bills with solar generation | Drives distributed solar adoption, reduces energy costs for factories and commercial users |

| CGPP (Corporate Green Power Programme) | Allows corporations to procure renewable energy from solar developers | Critical for ESG compliance, especially for MNCs and export-oriented manufacturers |

| CRESS (Corporate Renewable Energy Supply Scheme) | Expands access to renewable supply via third-party arrangements | Improves market flexibility, making Malaysia more competitive vs Vietnam’s DPPA |

| Solar MADANI / Solar ATAP | Government-led rooftop solar push for public and commercial sectors | Accelerates adoption and builds visible national momentum in solar deployment |

| Green Electricity Tariff (GET) | Allows consumers to subscribe to renewable energy via utility | Provides a low-barrier ESG entry point for companies without direct solar access |

| ENEGEM (ASEAN Power Grid positioning) | Malaysia as a regional electricity trading hub | Positions Malaysia as a cross-border energy player, not just a domestic market |

| Hydrogen Economy (Sarawak-led) | Development of green hydrogen production and export | High-value future energy export sector, especially for Japan and Korea demand |

| CCUS (Carbon Capture, Utilisation and Storage) | Carbon capture projects led by energy players like PETRONAS | Critical for heavy industry decarbonisation and maintaining relevance in oil & gas transition |

| EV Ecosystem & Industrial Electrification (BYD entry) | Expansion of EV supply chain and electrification demand | Signals future electricity demand growth, attracting manufacturing and battery ecosystem investments |

Taken together, this is not a weak or immature market story.

It is a country building:

- Policy depth

- Industrial alignment

- Renewable infrastructure

- Future-facing energy capacity

The problem is that this is not being translated clearly enough into a global narrative. This is exactly

Why Malaysia’s Policies Are Not Surfaced by AI

A lot of Malaysia’s strongest energy progress exists in places that are important, but not always highly visible outside the country.

Much of the information sits in:

- Policy PDFs

- Ministry or agency portals

- Press releases

- Domestic media coverage

- Event announcements and updates

That creates a visibility problem, while AI and Google do absolutely source from official government announcements because it is the most authoritative source, AI systems still prefers content that is :

- Most visible

- Most repeated

- Most cited

- Most easy to extract

And right now, Malaysia’s progress is often harder to “see” in that system than it should be.

Why Vietnam Leads the Green Energy Narrative

Vietnam’s narrative lead did not happen by accident, we have noticed that the country has done an excellent job on international visibility.

1. Vietnam Fits the “China + 1” Story Better in Global Coverage

Vietnam has become one of the clearest beneficiaries of the “China + 1” manufacturing shift.

ASEAN and UNCTAD data show that Southeast Asia has been attracting supply-chain-related investment, while analysis on Vietnam specifically points to its growing role as a manufacturing diversification base closely linked to Chinese and global supply chains.

That matters for green energy perception because once a country becomes central to manufacturing expansion, the next question is obvious: can it power that growth?

Vietnam’s renewable energy story therefore gets folded into a much bigger business narrative:

- Manufacturing relocation

- Export competitiveness

- Industrial electricity demand

- Long-term investor confidence

2. Vietnam’s Need for Power Is Easy to Understand

Vietnam’s power story is also easier for foreign readers to grasp because the demand pressure is so explicit.

The IEA notes that under Vietnam’s PDP8 pathway:

- Electricity demand is expected to double by 2030

- This is expected to rise fivefold to nearly 1,200 TWh by 2050

Vietnam’s revised PDP8 also raised its ambition, with major increases in projected power capacity and stronger renewable targets.

That creates a very clean narrative:

Vietnam needs a lot more electricity very quickly = Renewables are a core part of the answer.

This kind of story travels well internationally because it is simple, strategic, and commercially relevant.

3. Vietnam Has a Stronger International Narrative Layer

Vietnam also benefits from having an English-language media and business-information ecosystem.

One specific media agency we like to mention is VnExpress International, their target audience is clearly:

- English language speakers

- International audience

- Focused on gathering clicks and eyeballs through narrative framing

Even when foreign investors do not read Vietnamese policy documents directly, they are likely to encounter Vietnam’s story through English-language reporting.

Malaysia does have English-language news through Bernama, The Star, FMT and other outlets, including international and world sections.

But we have no one unified news portal that screams “This is for global investors”, even The Edge is regional-market based, not international.

4. The Narrative Disadvantage for Malaysia

When Vietnam’s energy story is told repeatedly through international business and policy coverage, foreign investors begin to associate the country with:

- Urgency

- Scale

- Industrial readiness

- Renewable momentum

Malaysia, by contrast, may have stronger policy depth in some areas, but it is more often interpreted through third-party coverage from outlets such as Bloomberg, CNN, or CNA.

That means Malaysia’s story is more often filtered than defined.

We don’t get to shout out Malaysia’s own accolades and achievements, third-party sites do it based on their own agenda and framing.

The result is a real narrative disadvantage.

Is Malaysia Ahead or Behind the Green Energy initiative

Now perhaps Malaysia really doesn’t deserve the top spot compared to Vietnam or Thailand or Philippines, nor are we trying to discount the country’s genuine initiative.

They have earned their places rightly so, and kudos to them.

But our objective as a PR agency is “How do we put Malaysia in the conversation?

Let’s look at the data:

| Metric (2026) | Malaysia | Vietnam | Philippines |

|---|---|---|---|

| Near-Term RE Target | 31% (2025), 40% (2035) | ~30%+ range (policy varies under PDP8) | 35% by 2030 |

| Long-Term RE Vision | 70% RE capacity by 2050 (NETR ambition) | Net zero roadmap evolving, strong but evolving | Net zero target (2050) |

| Installed RE Momentum | Moderate, structured rollout (LSS, NEM, CGPP) | Rapid solar surge (~17+ GW early scale) | Growing but smaller base (~2–3 GW solar) |

| Grid Reliability & Stability | Peninsular Malaysia has been reported with 28–36% reserve margin projected (2024–2030) | Curtailment issues in high-solar zones | Moderate, fragmented grid |

| Policy Structure Depth | Highly structured (NETR, NEM, LSS, CGPP, CRESS) | Aggressive but less layered | Growing frameworks |

| Corporate Energy Access | Expanding (CGPP, CRESS, GET) | Strong (DPPA-style access) | Improving |

| Industrial Integration | Strong (Penang, Johor, Sarawak, data centres) | Strong manufacturing pull | Moderate |

| Energy Demand Growth Story | Stable, managed growth | Explosive demand (doubling by 2030) | Growing demand |

| Global Narrative / Visibility | Low, fragmented across local channels | High, repeated in global media + reports | Medium |

| Investment Pipeline Signals | $10B+ RE MoU (ACWA), NETR pipeline active | Large planned capacity expansion | Large long-term targets |

Conclusion: What Should Malaysia Do Now?

At PRESS PR Agency, we see this gap clearly.

Malaysia already has a strong green energy story. The challenge is that it isn’t being amplified in the right places, or in the right format, to influence global perception.

Our Digital PR services work with government bodies, GLCs, and industry leaders to:

- Translate policy and technical progress into clear, investor-facing narratives

- Build international media visibility beyond domestic coverage

- Structure content for AI discovery, search, and long-term authority

- Position Malaysia as a credible, competitive player in the global green energy conversation

Because ultimately, this is not just about communications.

It’s about making sure that when the world asks where the next green investment should go, Malaysia is part of the answer, not an afterthought.

Disclaimer: This opinion piece is intended for general discussion and does not represent investment advice or an official assessment of any country’s energy sector. All comparisons are based on publicly available information and are presented to illustrate how narratives shape investor attention.

Source:

- Bridgewise — “78% Now Use AI for Investment Information, Bridgewise Global Study Finds” (press release / survey highlights, 2026)

- Bridgewise — “The State of AI for Wealth in 2026” (blog / expanded context incl. “65% likely to replace some research,” 2026)

- Fintech Global — “78% of investors now use AI for research” (third-party coverage of Bridgewise findings, 16 Apr 2026)

- SEDA Malaysia — MyRER (Malaysia RE targets 31% by 2025; 40% by 2035) —

- Government of Malaysia (EPU/Ministry of Economy) — National Energy Transition Roadmap (NETR) PDF (incl. 70% installed RE capacity by 2050 ambition) —

- IRENA — “Malaysia Energy Transition Outlook 2023” PDF (context and reinforcement for Malaysia transition pathway)

- SEDA Malaysia — Net Energy Metering (NEM) programme portal

- Suruhanjaya Tenaga (Energy Commission, Malaysia) — CGPP guide PDF (Corporate Green Power Programme) —

- Single Buyer (Malaysia) — CRESS programme page (Corporate Renewable Energy Supply Scheme)

- myTNB / Tenaga Nasional Berhad — Green Electricity Tariff (GET) programme page

- Suruhanjaya Tenaga (Energy Commission, Malaysia) — ENEGEM / Energy Exchange Malaysia page (incl. CBES cap details)

- IEA — “Achieving a Net Zero Electricity Sector in Viet Nam” (executive summary; PDP8 demand doubling by 2030 and ~fivefold by 2050)

- IRENA — Viet Nam Renewable Energy Statistical Profile (solar capacity reference used for “scale” claim)

- Philippines Department of Energy (DOE) — Power Development Plan category page (RE targets 35% by 2030; 50% by 2040) —

- Reuters — “Saudi Arabia’s ACWA Power signs MoU to develop renewables capacity in Malaysia” (up to $10B initial investment / capacity plan context; 29 May 2025)

- TNB (newsclip PDF on reserve margin / adequacy context used for grid stability proxy; 19 Mar 2024)

{kind=link}