You finally get that salary increase. Maybe it comes from a promotion, a job switch, or a growing business.

At first, nothing dramatic changes. You just make a few upgrades. Better meals, more frequent Grab rides, maybe a new phone, or nicer clothes. Everything feels reasonable.

Then slowly, your baseline shifts. What used to feel occasional becomes normal. What used to feel like a treat becomes the standard.

A year later, your income is higher, but your finances feel almost the same.

This is lifestyle inflation, and it is one of the most common reasons people earn more without building much more wealth. It does not feel reckless, which is exactly why it is dangerous.

What Is Lifestyle Inflation?

Lifestyle inflation is when your spending increases as your income increases, leaving little or no improvement in savings or long-term wealth.

It is also known as lifestyle creep. The change is usually gradual rather than dramatic. As income rises, expectations and habits often rise with it.

That means your earning power improves, but your financial position does not improve by much.

In simple terms, you are moving forward in income, but not really getting ahead.

Why Lifestyle Inflation Matters in Malaysia

Lifestyle inflation can hit harder in Malaysia because higher income often meets higher commitments very quickly.

Several local factors can amplify the effect:

- Living costs remain a real concern, especially in major urban areas

- Car upgrades can significantly raise fixed monthly costs through instalments, insurance, and maintenance

- Instalment-based financing can make upgrades feel manageable in the short term, even when total commitments rise

- Malaysia’s digital payment ecosystem makes spending easier, faster, and less noticeable

This matters even more because many households already carry meaningful financial commitments. In Malaysia, household debt remains high, which means lifestyle inflation often builds on top of existing obligations instead of starting from zero.

Retirement planning also adds pressure. EPF has introduced clearer retirement adequacy benchmarks, which shows that long-term security requires more than simply letting income rise and hoping that savings will sort themselves out.

When lifestyle inflation enters this environment, it becomes much harder to build resilience, flexibility, and real wealth.

How Lifestyle Inflation Works

Lifestyle inflation is not one big decision. It is a pattern that builds over time.

It usually follows this sequence:

- Income increases through career growth or business growth

- Spending rises in response

- New habits form around that higher spending

- Fixed costs increase and become harder to reverse

- Savings and investing do not rise meaningfully

What makes this dangerous is that each step feels justified. There is rarely a clear moment where it feels like you made a bad financial choice.

But over time, the result becomes obvious. You are earning more, yet your financial flexibility has barely improved.

Key Aspects of Lifestyle Inflation

The Fixed Cost Trap

The biggest risk is raising your fixed monthly commitments.

These often include:

- Car loans with higher instalments

- Mortgage or rental upgrades

- Insurance linked to higher-value assets

- Subscription services that slowly stack up

Fixed costs are the most dangerous form of lifestyle inflation because they are not easy to undo. A one-time purchase hurts once. A fixed commitment can affect your cash flow every month for years.

The Lifestyle Baseline Reset

Your definition of “normal” keeps moving upward.

What once felt like a luxury starts to feel expected:

- Dining out occasionally becomes a regular habit

- Budget travel becomes premium travel

- Basic products begin to feel “not good enough”

This reset is powerful because it changes how you think. You stop seeing the upgrade as optional and start seeing it as standard.

The Convenience Economy Effect

Modern spending is easier and faster than ever, which makes it easier to overlook.

In Malaysia, this often shows up through:

- Food delivery platforms

- E-wallet and cashless payments

- Subscription-based services

- One-click online shopping

Because many transactions are fast, small, and frictionless, it becomes easier to underestimate how much your monthly baseline has risen.

The Social Comparison Loop

Spending is often influenced by what you see around you.

Examples include:

- Colleagues upgrading their cars or homes

- Friends dining at more expensive places more often

- Social media making a certain lifestyle look normal

This creates subtle pressure to keep up, even when your priorities should be different.

Real-Life Examples in Malaysia

Lifestyle inflation becomes easiest to spot when you look at ordinary, relatable situations.

The Car Upgrade Cycle

You start with a practical car. Then income rises, and upgrading feels deserved.

Soon:

- The monthly instalment increases

- Insurance costs go up

- Maintenance becomes more expensive

What felt like a reward becomes a larger fixed monthly structure.

The Housing Upgrade Effect

You move from shared accommodation or a simpler unit into a nicer condo or better location.

Then the real cost expands:

- Higher rent or mortgage

- More furnishing expenses

- Higher maintenance and utility costs

- A lifestyle that fits the upgraded environment

The move does not just raise housing cost. It often raises surrounding spending too.

The Daily Convenience Habit

Nothing looks serious on its own:

- Ordering food instead of cooking

- Regular café purchases

- Paying for multiple streaming apps

- Frequent small online orders

But when repeated often, these small expenses build a much higher monthly baseline than most people realise.

The Income Trap Scenario

A simple example:

- Salary increases by RM1,000

- Spending increases by RM900

- Savings rise by only RM100, or not at all

That is lifestyle inflation in its clearest form. Income improved, but financial progress barely moved.

Why Lifestyle Inflation Is a Bad Thing

Lifestyle inflation is harmful not because spending is wrong, but because it can quietly block financial progress.

It Neutralises Income Growth

You earn more, but your financial position does not improve much.

This is one of the most frustrating outcomes of lifestyle inflation. On paper, you are doing better. In practice, you may still feel financially tight.

It Delays Major Financial Milestones

When more money is absorbed into lifestyle upgrades, it becomes harder to save for:

- A property down payment

- Investments

- Business opportunities

- Retirement

Progress slows because your increased income is no longer being used to build assets.

It Increases Financial Vulnerability

Higher monthly obligations mean:

- Less flexibility in an emergency

- More stress during income disruption

- Less room to adapt when costs rise

A person with lower fixed commitments is often more financially resilient than someone who earns more but has locked in too many ongoing expenses.

It Weakens Long-Term Wealth Building

When more of each pay raise goes to spending instead of saving or investing, you reduce the long-term benefit of compounding.

That is the hidden cost. It is not just about what leaves your account today. It is also about what never gets the chance to grow.

The Hidden Cost: Opportunity Cost and Compounding

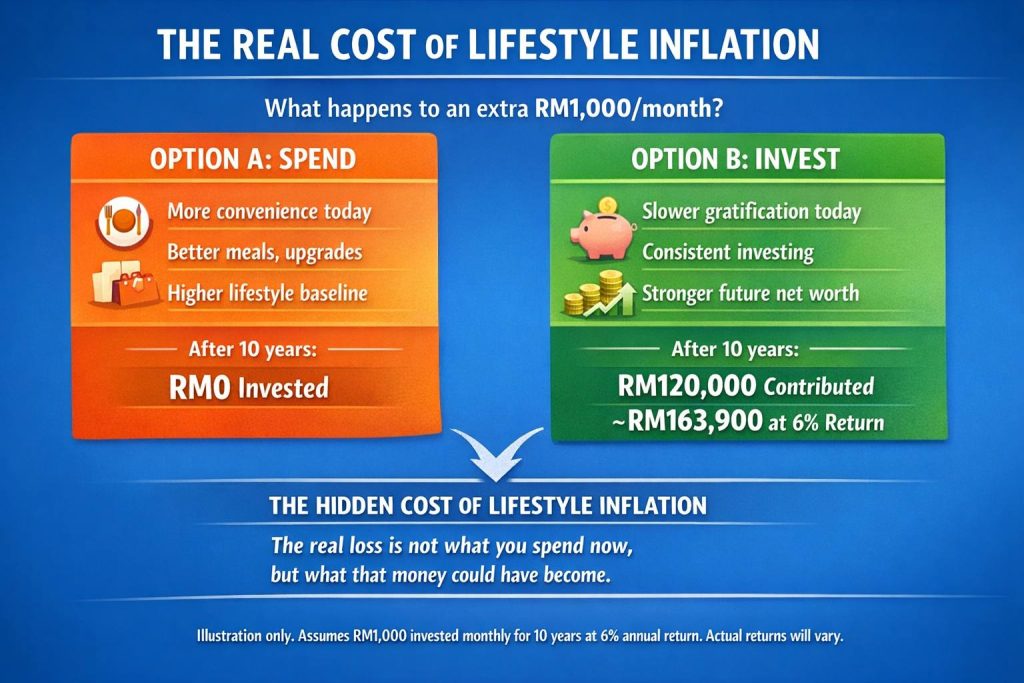

The biggest loss from lifestyle inflation is often invisible. It is the wealth you never build.

Think about two scenarios:

- Scenario A: a RM1,000 income increase gets fully absorbed into spending

- Scenario B: that RM1,000 is regularly saved or invested

At first, the difference may not feel dramatic. But over time, even moderate returns can create a very large gap.

That is why lifestyle inflation becomes expensive. The real cost is not just higher spending now. It is the future value you gave up.

Lifestyle Inflation vs Cost of Living

Not every increase in spending is lifestyle inflation.

This distinction matters.

Cost of Living Increase

This is driven by external factors such as inflation and higher prices for essentials.

Examples include:

- Food

- Rent

- Utilities

- Transport costs

These are not always within your control.

Lifestyle Inflation

This is driven by personal choices and upgraded spending habits.

Examples include:

- Moving into a more expensive home than necessary

- Upgrading to a higher-cost car

- Making convenience spending a permanent habit

- Turning occasional luxuries into normal monthly costs

Understanding the difference helps you be fair to yourself while still taking responsibility for what you can control.

How To Stop Lifestyle Inflation

The goal is not to stop enjoying life. The goal is to make sure income growth improves your financial life, not just your spending level.

Increase Your Savings Rate With Every Raise

Do not wait to see what is left over.

A simple rule is to direct part of every raise straight into savings or investments first. For example, you could commit to saving at least 50 percent of any income increase.

That way, a better income automatically improves your financial position.

Create a Spending Ceiling

Decide what level of lifestyle is enough for now.

This does not mean never upgrading. It means not allowing every income increase to automatically become a lifestyle increase.

A ceiling helps you enjoy progress without letting expenses expand endlessly.

Automate Financial Decisions

Move money before you can casually spend it.

Examples include:

- Automatic transfers to savings

- Scheduled investment contributions

- Separate accounts for goals

Automation reduces the need to rely only on discipline.

Define Clear Financial Targets

Spending becomes easier to control when your money has a clear job.

Useful targets might include:

- Emergency fund goals

- Investment milestones

- Travel fund goals

- Retirement savings targets

When your goals are specific, unnecessary upgrades become easier to question.

Track and Audit Your Expenses

Lifestyle inflation often hides inside routine spending.

Review your expenses regularly and look for creeping costs such as:

- Subscription services you barely use

- Convenience spending that has become automatic

- Upgrades that no longer feel noticeable

Small recurring costs deserve more attention than occasional large purchases.

Delay Major Upgrades

Not every upgrade needs to happen immediately.

Introduce a waiting period before large purchases or new monthly commitments. A pause creates space to ask:

- Do I really need this?

- Will this improve my life meaningfully?

- Am I buying this for function, convenience, or image?

A short delay can prevent long-term regret.

Healthy vs Unhealthy Lifestyle Inflation

Not every lifestyle upgrade is bad. The difference is whether it creates long-term value or long-term burden.

Healthy Upgrades

These often improve your future position:

- Education and skill-building

- Health and well-being

- Tools that improve productivity

- Spending that increases earning power

Unhealthy Upgrades

These often create pressure without much lasting value:

- Status-driven purchases

- High fixed-cost commitments

- Convenience habits that become permanent

- Lifestyle upgrades made mainly to match others

Intentional spending is very different from automatic spending.

A Simple Framework: Grow Wealth Faster Than Lifestyle

A useful rule is this: let your wealth grow faster than your expenses.

A simple approach:

- Increase income

- Increase savings and investments first

- Upgrade lifestyle only with the remaining portion

This keeps financial progress moving in the right direction even as your standard of living improves.

Control Lifestyle, Not Just Income

Lifestyle inflation is one of the most overlooked financial traps in Malaysia. It rarely feels like a mistake, but over time it can quietly block savings, reduce flexibility, and weaken long-term wealth building.

The real issue is not whether you spend more as you earn more. The real issue is whether your financial future improves too.

As your income or business grows, how you shape your financial story matters just as much as the numbers themselves. At PRESS PR Agency, we help individuals and brands build credibility, trust, and long-term growth through strategic PR that strengthens the story behind their success. Contact PRESS, your most reliable PR agency in Malaysia, today to learn more.

Disclaimer: This article is for general educational purposes only and does not constitute personalised financial, investment, or legal advice. Always assess your own situation carefully and consult a qualified professional before making major financial decisions.

{kind=link}